The Quantum Decade: Reading from 2026-2036

File 1 of 3: Global projections for quantum computing and AI, in business terms.

Prepared June 2026

NOTE: I came to this without a physics degree, without a research budget, and in the middle of years that included loss I didn’t plan for. I’ve spent forty two years in technology as a bridge, sometimes a builder, mostly moving between the people who understood systems and the people who had to use and govern them.

When Google’s Willow chip made headlines in winter of 2025, I did what I’ve always done: I followed the thread until I understood it well enough to be useful. What you’re reading is a part of nine months of that work, written by someone who’s earned any authority the slow way, by paying attention until something becomes clear.

Why this briefing exists

If you lead a company today, you have spent the last three years getting your arms around AI. You do not have spare attention for another paradigm shift. Unfortunately, the next one is already underway, and it intersects directly with the AI decisions you are making right now.

Quantum computing crossed a line in the past eighteen months. It moved from physics experiment to commercial market. McKinsey’s Quantum Technology Monitor 2026, published in April, calls it a commercial tipping point, and the numbers back the label: investment in quantum technology startups reached $12.6 billion in 2025, a 6.3x increase over 2024.

Quantum computing companies generated more than $1 billion in revenue worldwide in 2025, with projections reaching as high as $4.4 billion by 2028. More than 300 global companies, including Airbus, JPMorgan Chase, Boehringer Ingelheim, and Liberty Mutual, are actively collaborating with quantum technology providers on real business problems.

This is not a technology you need to deploy this year. It is a technology you need to understand this year, because two of its consequences arrive on your doorstep well before the machines do:

A cybersecurity transition that is already mandated by governments worldwide

A competitive dynamic where early movers lock up talent, partnerships, and intellectual property

Where quantum actually stands, June 2026

Strip away the hype and the field looks like this:

Hardware is advancing on multiple fronts, but critically, fault tolerance is not here yet.

IBM has published a detailed plan for a large-scale fault-tolerant quantum computer by 2029.

Google demonstrated its Quantum Echoes algorithm on the Willow chip in late 2025, a verifiable quantum advantage on a molecular simulation task.

Microsoft announced its improved Majorana 2 topological chip this month, citing a thousandfold reliability improvement and an accelerated road map.

Most major players target roughly 100 to 200 logical qubits by 2030. These road maps are credible but not guaranteed; qubit counts alone do not equal useful computation.

The near-term value is hybrid.

Nobody serious expects quantum computers to replace classical ones. The working model is hybrid: classical high-performance computing handles the bulk of a workload, AI orchestrates, and quantum processors take on the narrow, fiendishly complex subproblems where they have an edge.

This architecture is already being tested in production settings at financial institutions and pharmaceutical companies.

The money has shifted from governments to private capital.

In 2024, a third of quantum startup investment came from public sources. In 2025, just 3% did. Roughly 60% of 2025 investment concentrated in the top ten deals, and consolidation has begun, including IonQ's $1.1 billion acquisition of Oxford Ionics.

When private capital concentrates this fast, a market is forming, not a science fair.

Access is through the cloud, not the loading dock.

Mid-size companies will never buy a quantum computer; they cost millions to tens of millions each. They will rent quantum capacity through quantum-as-a-service platforms such as Amazon Braket, IBM Quantum, and Microsoft Azure Quantum, the same way they rent GPU capacity for AI today.

McKinsey found that private companies overwhelmingly favor this hosted model, and it is the entry point that matters for organizations your size.

For ongoing tracking, the Quantum Computing Report and The Quantum Insider both maintain credible, frequently updated news feeds. (More on sources in File 3 of this series.)

Quantum and AI: why these stories converge

The instinct is to treat quantum as a separate technology wave that arrives after AI. The better mental model is that quantum becomes a specialized accelerator inside the AI-era computing stack you are already building.

Three convergence points matter for business planning:

Shared infrastructure

The data pipelines, cloud architecture, and governance you are building for AI are the same foundations quantum workloads will run on. Companies modernizing their stacks for AI are, mostly without realizing it, doing the prerequisite work for quantum. The reverse is also true: a brittle, undocumented data environment will block both.

Shared talent model

The skill in shortest supply is not quantum physics. It is translation: people who can map a business problem to the right computational tool, whether that tool is a large language model, a classical optimizer, or eventually a quantum processor. McKinsey notes that demand is growing for engineers, developers, and business experts who can translate quantum capability into application, not just for physicists.

Mutual acceleration

AI is now being used to design quantum hardware (Microsoft credits agentic AI with helping develop its latest chip), and quantum simulation is expected to improve the training data and chemistry models that feed AI. Each technology shortens the other’s timeline, which is one reason expert estimates of Q-Day (more on that in File 2) keep moving earlier rather than later.

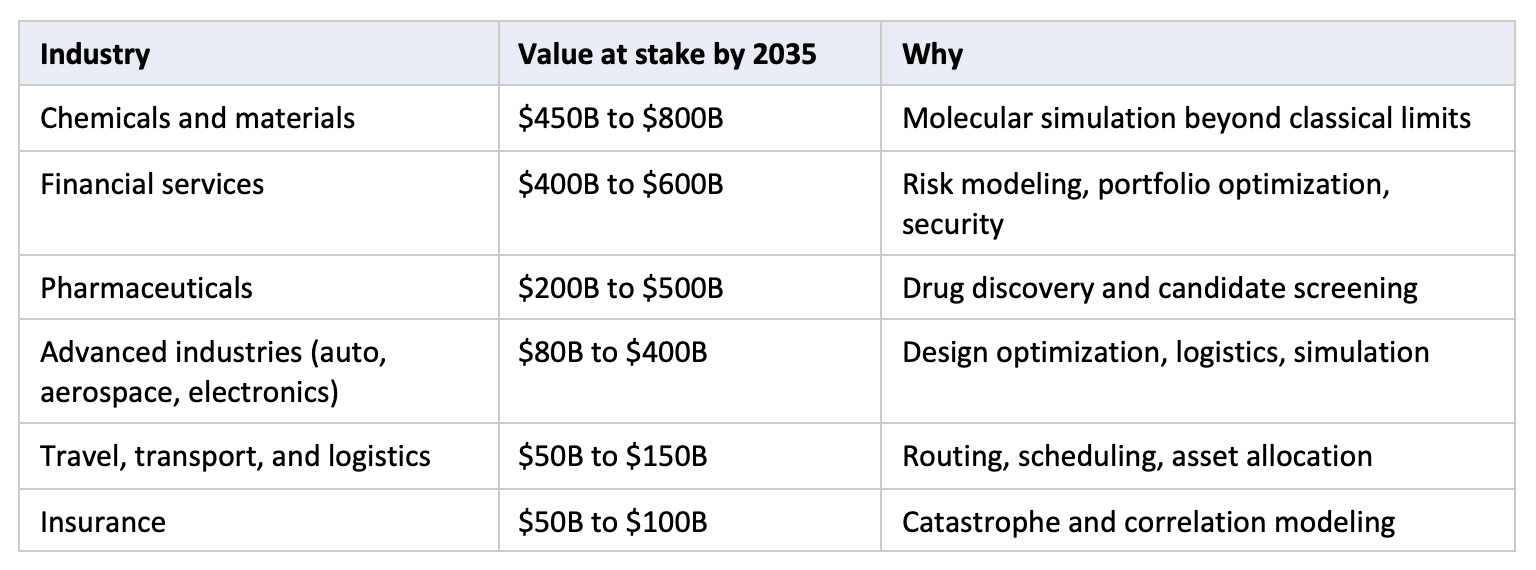

The economic picture through 2035

McKinsey’s updated analysis puts the value at stake from quantum computing at $1.3 trillion to $2.7 trillion worldwide by 2035, concentrated in industries with hard computational problems:

Two honest caveats here.First, these estimates overlap with generative AI’s impact; the value is not fully additive. Second, McKinsey itself flags that near-term return on investment remains difficult to quantify, with most applications still experimental or hybrid. Treat these figures as a directional signal of where computational advantage will land, not as a forecast you can bank.

A third caveat, because forecasts deserve triangulation: not everyone agrees on the size of the prize. Boston Consulting Group’s most recent forecast projects $450 billion to $850 billion in economic value, on a longer horizon (2040), with a provider market of $90 billion to $170 billion.

That is well under half the McKinsey figure with five extra years to get there. BCG also marked down its estimate of value from today’s pre-fault-tolerant machines to a few hundred million dollars a year, a sobering counterpoint to others’ tipping-point language.

The two firms use different methodologies and the spread between them is the honest signal: the direction is agreed, the magnitude is not.

For planning purposes, the BCG floor is high enough to justify the modest preparation this series recommends, and the McKinsey ceiling is uncertain enough that it should not justify more.

If your company is not in those industries, the value will still reach you through your supply chain, your bank, your insurer, and your software vendors, all of whom are in those industries.

A picture of 2036

Forecasting a decade out is a hazardous sport, so consider this a plausible composite drawn from current road maps, government migration timelines, and investment patterns rather than a prediction.

Here is what 2036 likely looks like for a mid-size company, written from the perspective of someone negotiating 2026 concerns:

Quantum is a line item, not a moonshot.

You buy quantum-accelerated capability the way you buy cloud AI today: through a service subscription, embedded in vertical software for logistics, finance, or R&D. You may pay for outcomes (a viable molecule, an optimized network) rather than compute time. You probably don't know, or care, which computations ran on quantum hardware, just as you don't likely know which of today’s services run on GPUs versus CPUs.

The encryption transition is finished for the prepared and expensive for the rest.

Government mandates worldwide converge on 2030 to 2035 for migration to post-quantum cryptography. By 2036, organizations that started in the mid-2020s completed the move as routine infrastructure work. Those that waited paid emergency-project prices, and some learned that data stolen in the 2020s under harvest-now-decrypt-later attacks was readable all along.

Fault-tolerant machines exist but remain scarce and specialized.

If IBM, Google, and their peers hit their road maps even approximately, early fault-tolerant systems arrive between 2029 and the early 2030s. By 2036 they are doing genuinely new work in materials, chemistry, and optimization, but capacity is rationed and expensive, accessed almost entirely through cloud platforms and consortium arrangements.

Quantum sensing arrives through the side door.

The quietest of the three quantum fields (computing, communication, sensing) shows up in navigation that works without GPS, medical imaging, and infrastructure inspection. You’ll encounter it as a feature of products you buy, not a technology you adopt.

Competitive sorting has already happened.

The firms that built translation capability and ran disciplined pilots in the late 2020s hold the patents, the vendor relationships, and the institutional knowledge. The cost of entry rose every year they were learning and others were waiting. This is the same movie the industry watched with cloud and then with AI, on roughly the same reel length.

The honest uncertainty

Timelines could slip. The hard constraints now are engineering and supply chain (cryogenics, lasers, control electronics, manufacturing) rather than pure science, and those constraints yield to capital and time, but not on command. Some announced road maps will be missed. A few well-funded companies will fail.

It is also worth knowing that the most rigorous independent assessment of the field is consistently more conservative than the consultancies and the vendors. Olivier Ezratty’s Understanding Quantum Technologies, a free 1,500-page reference updated annually since 2018, catalogs every qubit modality, vendor road map, and use-case claim, and routinely finds the timelines optimistic and the benchmarks softer than the press releases suggest.

Reading even its 38-page key-takeaways edition alongside the McKinsey and BCG material is the fastest way to calibrate. The pattern I found across all three sources: agreement that the transition is real, disagreement about pace and magnitude.

What does not change under any plausible scenario: the cryptographic transition is mandated and underway regardless of when Q-Day arrives, hybrid quantum-classical computing is already producing early commercial value, and the cost of learning rises as the ecosystem consolidates.

The prudent posture for a mid-size company is not investment in quantum hardware. It is literacy, a security plan, and a watching brief with teeth.

My next post covers exactly how we can begin to build that posture.

This is File 1 of 3 in The Quantum Briefing.

File 2: Preparing for the Quantum Era: A Practical Roadmap

File 3: Quantum Computing: A Curated Resource Guide

Don’t leave your AI or quantum journey to chance.

Connect with us today for your AI adoption support, including AI Literacy training, AI pilot support, AI policy protection, risk mitigation strategies, and developing your O’Mind for scaling value. Schedule a bespoke workshop to ensure your organization makes AI work safely and advantageously for you.

Your next step is simple. Let’s talk together and start your journey towards safe, strategic AI adoption and deployment with AIGG.